Today I received an email titled “You have 25% off all Lyft Line rides”.

You’ve got a 5-star rating, and that’s worth celebrating. Your Lyft Line rides are now 25% off until 1/28

Today I received an email titled “You have 25% off all Lyft Line rides”.

You’ve got a 5-star rating, and that’s worth celebrating. Your Lyft Line rides are now 25% off until 1/28

Try Canada Box

Last October I wrote a post on Try The World deals. I like the box enough to review them so I will start with the recently received Canada box. This box contained 8 items among which 2 were duplicates and there were no non-veg items.

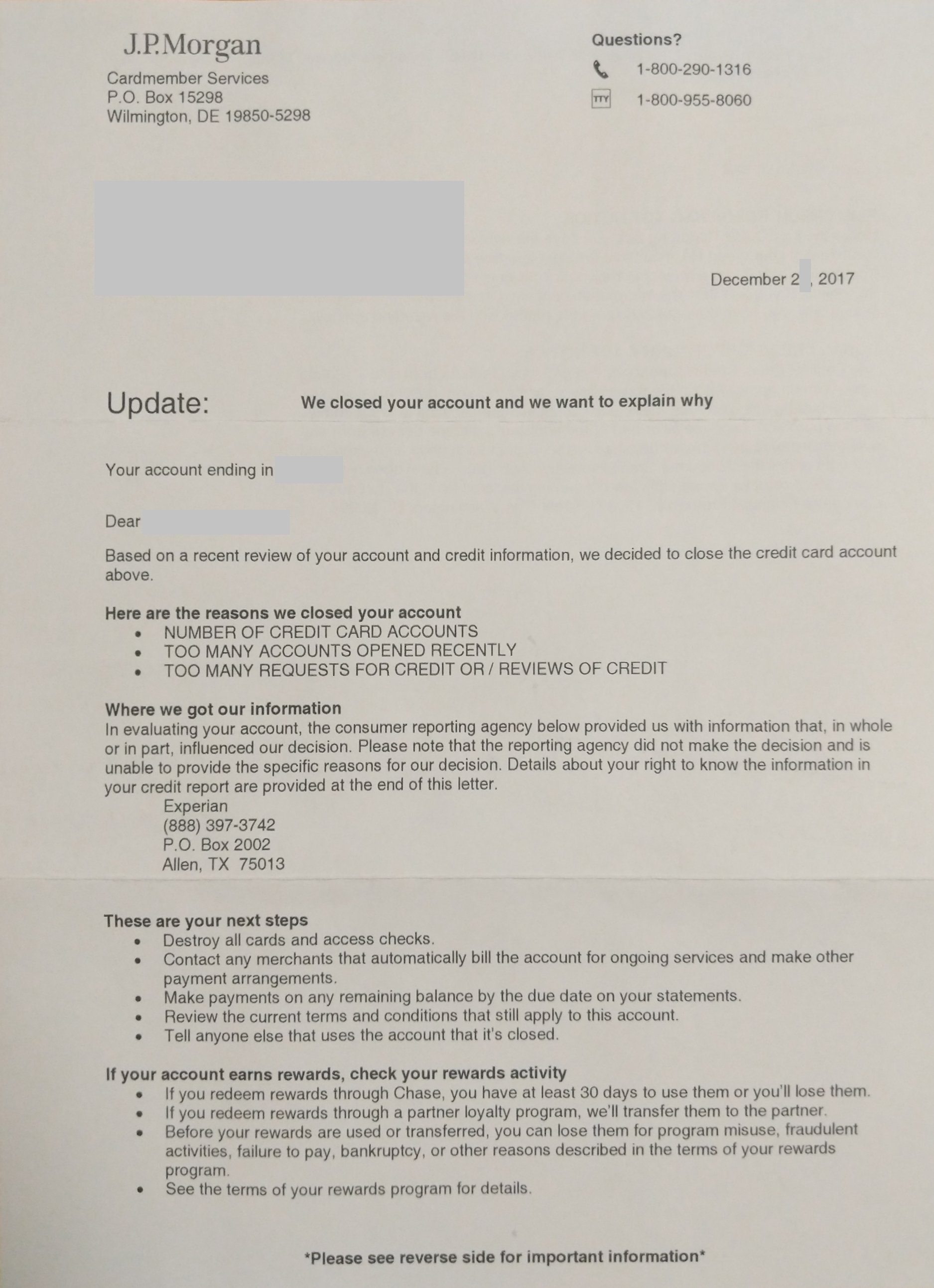

Update: for a while now I’ve replaced Chase referral links on this site to those of my family members. I’ve also cashed out a good chunk of UR. I guess that tells you what I think my odds are.

Typically Chase credit card shutdowns were related to doing something like anonymous bill payment, selling points, and maxing out 5x categories through MS. But as of late DPs indicating new type of shutdown has been floating around and it has nothing to do with above listed reasons.

This new type of Chase shutdown is a result of the following:

I’m not making this up nor am I making an educated guess on these reasons. Above listed reasons are the official reason given in the Chase shutdown letter.

So why does this matter and why is this a big deal?

Previously if you did not do fishy stuff like anonymous bill payment, selling points, etc then you were pretty much on the safe side. But this new reason for shutdown clearly indicates that even if you don’t do those things you may not be on the safe side.

However, there are two good news. First, decent number of these shutdowns have been reversed but the fact that not all were reversed is worrying. Second, 100% of these types of shutdown happen after one applies for a Chase credit card (business or personal does not matter).

I believe that when an analyst sees a messy credit report during review of a credit card application, s/he hits a “review this bastard” button and sends the file somewhere else to be reviewed. I believe they’re training analysts differently now otherwise reports of this type of shutdown would have existed a year ago.

Above hypothesis is supported by my own case as I was shutdown after several days of applying for a Chase card. How much is “several days”? This time span can shortly detailed as such (1) Chase send me a letter regarding my application (2) I sent Chase a response letter (3) Chase, having reviewed my letter, sent me another letter (4) few days later I call, sort everything out, and I am told that my application needs further review (5) a day or two later all my cards are shutdown. My point being, if it was automated I would have been shut within few days of Chase pulling my credit report. It was a clear case of someone reviewing my app and going “fuck this guy”.

Banks change the rule and you must change with it. You must give up on the old ways and adopt with changing times. Unfortunately, when rules change some churners like me end up being the data point. Fortunately for you, here is my breakdown of how you can avoid same thing from happening to you:

I would also somewhat encourage people to

A good portion of these shutdowns have been reversed but that does not mean you’ll have a positive outcome. Additionally one must keep in mind that the DPs on this type of shutdown have been in the range of 10-20 and we’ve only had a chance to peek at less than 3-4 irreversible shutdowns.

I recently saw a Chase shutdown DP of a regular churner with 10+ Chase credit cards and his shutdown was irreversible. This was the closest DP I had to mine and I thought to myself “if he had no change, what change do I have”?

I was positive that I could turn this shutdown around for myself but the further I talk with Chase the further I realize that this is a losing battle for me. However, I must say that 2 irreversible shutdown DP from regular churners does not prove all regular churners will be doomed in this case.

While I hope another regular churner in my shoe would have a better luck than I, the reality is that if you’re tons of inquiries and accounts then it is going to be really difficult to convince an analyst that you have any good intention. The only option churners like myself have is to be honest and admit that we’re just gaming status and points but that did not take me very far. I found that throwing in some keywords were helpful than other but maybe that is a topic for different day.

Anyway, to cut things short, my point is –

Long story short – I don’t know. Chase has been transparent to me about shutdown reason from day one but that is not like them. This made me believe that this is a “soft ban” and I should be allowed to get more cards in the future.

Also, Both my personal and business checking accounts are intact. When I asked if checking accounts would be shutdown, I was told something along the lines of “they haven’t been so far”. I have also been told by multiple chase representatives that I should be able to get more cards but when I questioned them on it, it was clear that none of them were certain.

I was sure that eventually Chase would welcome be back (i.e. this is a soft ban), well, until I received a letter stating why I was denied for the card I had applied for – “previous unsatisfactory relationship with this bank”.

I think this means that unless this ban is overruled (unlikely because of my profile) I’m done with Chase for life. It has been known that “previous unsatisfactory relationship” is known to eventually transfer over from credit card to banking and vice versa. Again nobody at Chase has confirmed this nor denied it nor have I seen a DP in this regard of anyone who has been shutdown for this reason.

P.S. if you’re new to this blog and curious about what cards I have, how often I churn, how rapidly do I apply, etc, then check my churning summary for year one (2016) and year two (2017). If that does not suffice, you may also check out Denials are Lessons #1, Learning from Denials #2, and Learning from Denials #3.

When Project Fi was introduced in 2015 it was a cool concept at a cheap cost but for quite some time now other cell phone carriers have outdone Fi in pricing. Today Project Fi announced Bill Protection which essentially makes Fi competitive for some people. If you’re a heavy data user or if you’ve a large family then you might want to take a look at Fi again.

after 30 days of active line, we’ll both get $20 Fi credit

or just use the code 5W5863

Traditionally Fi has charged $10/GB (domestic or international) which resulted in a heavy user paying hundreds of dollar for Fi service. Now because of bill protection one pays $10/GB until their “data level” is reached and any data consumed then after is free.

In other words, there is a hard cap on how much you can be charged regardless of the amount of data you consume. This capped price depends solely on the number of lines you have. The number of lines you have determines the maximum data cost your account can be charged. This information has been elegantly displayed in the chart below.

Example: 1 line

Example: 1 line

If you have one line you pay $20 for call & text and you would pay $10/GB for first 6 GB. After 6 GB “data level” threshold has been met, bill protection feature would kick in, make addition data consumed free, and preventing you from being charged above 6 GB “data level” threshold.

Example: 2 line

If you have two lines then you will pay $20 for call & text of first line while the second only costs $15. In this scenario you would pay $10/GB for first 10 GB and any additional GB consumed is free. Overall you would pay $20+$15 = $35 for call and text plus a maximum data cost of $100 thus netting you a maximum combined cost of $135.

Yes but as expected there is throttling. The first 15 GB is uncapped on each line, then after data speed is capped at 256 kbps until next cycle for the line that exceeded 15 GB threshold. If you don’t want to get capped at 256 then you can contact Fi and pay $10/GB.

The more lines you have the less it costs per line. For example, you pay $80 max for 1 unlimited line but for 6 unlimited lines one would on average pay $45.83/line. This information has been detailed out a table shared in a reddit post.

The other interesting sweet spot is that bill protection also works for international data (135+ countries) as well as data-only SIMs. Note that all data-only SIMs belonging to a single line share data restriction of said single line.

I really like that Fi has finally entered unlimited data space. Fi has needed change in pricing for very long and this might just have been the thing to keep it competitive with other carriers. I think unlimited plan will be handy for frequent international travelers or those who are travelling internationally for an extended period of time.

I personally have T-mobile 55+ plan for unlimited data so Fi’s unlimited plan is not appealing to me. I will continue to keep Fi as a backup eSIM.

I don’t know about you but I joined Simple when it was an invite only banking app. Back then they were selling it as an fee free online banking app that is smooth, fast, elegant, and yet simple. It was a cool app because back then online banking apps were a mess to look at. I remember being superbly pleased with this eye pleasing app that allowed me to lock debit card right away, transfer money instantly to other simple users, and had an easy option to send secure messages.

As you may know Google has placed Project Fi travel trolley vending machine at various airports (full list by google). The perk of living in Chicago is that both ORD and MDW is equipped with a Fi travel trolley but like any other vending machines, Fi travel trolley sometimes runs out of items or simply breaks.

UPDATE: This post was originally made on Dec 11, 2017 but I’ve refreshed it because deal will die tomorrow Jan 16th, 2018.

In order to get the code you need to be a Project Fi subscriber. You can read the details of this promo in google’s page by clicking here.

![[Targeted] UberEats 2 Week of Unlimited Free Delivery](https://i0.wp.com/travelinpoints.com/wp-content/uploads/2018/01/Uber_free_delivery.png?resize=1049%2C863&ssl=1)

Uber continues giving away freebies to acquire new customers. This time around they’re offering two week of unlimited free Uber Eats to certain new UberEATS customers. This is a targeted offer so check for email titled “Enjoy 2 weeks of free delivery!”

If you’re someone who uses UberEATS a lot then this is a great deal. Remember that the discount expires from the date you received the email.

It looks like Dosh $15 holiday referral bonus was a success because the same promo has returned for the new year. Dosh is offering a two week long $15 referral bonus which runs from Jan 7th to Jan 21st 2018 11:59 pm PT.

It looks like Dosh $15 holiday referral bonus was a success because the same promo has returned for the new year. Dosh is offering a two week long $15 referral bonus which runs from Jan 7th to Jan 21st 2018 11:59 pm PT.

for you: $5 for linking 1st card, $1 for 2nd card, and $1 for 3rd card

for me: $15 when you link your 1st card

https://link.dosh.cash/YCLI/HoBWZwqRQJ

In order to get the bonus, you must use above link to download the app.

In order to get the bonus, you need to use referral link and add a card before the promo period ends. When your balance is at $15, you can cash out directly to your bank account or to Paypal account.

You can read more about this promo by clicking here.

When this promo ran last time I know some of you instantly caught on what I was hinting at while others asked me how to maximize it. Back then the promo was extremely relaxed but unfortunately, on Dec 22nd 2017, Dosh ToS was updated to be more restrictive:

I personally also churn non-VoIP phone numbers so this is easy few bucks in my pant. You may find this to be easy money by referring friends and family members.

Recently I wrote a piece Robinhood is Amazing for Direct Deposit and I wholeheartedly recommend everyone to at least try Robinhood (RH). In that post I had presented a screenshot of Chase counting RH as a direct deposit (DD) but I had also mentioned that it won’t work anymore. However, there is an even more hardcore trick that triggers DD requirement literally everywhere including on Chase.

Chase direct deposit through Chase business checking

In this post I will talk about making DD through Chase business checking account. All you need to do is go to “send payment” tab and then to “ACH payments” menu. If you’ve never done this before then you would go to “add a payee” where you would be prompted a number to call 1-844-200-0624.

During the call you may be asked to either enroll in “ACH payments” option or “payroll”, I suggest you choose the prior one as the latter is getting phased out in a few months. The cost for this service is $25 a month but with this feature enabled you’ve the power to DD literally anyone. If you’re the type who manages multiple accounts (SO, parents, siblings, etc) then $25/month for such a powerful feature probably sounds like a fair deal to you.

Please note that during this call you’ll be asked couple of questions like “how often do you plan to use this feature?”, “how much $ do you plan to send through this feature each month?”, and perhaps even “do you see your business growing in the future?”. I would highly recommend trying to honestly answer these answers. If you end up pushing higher volume than what you state, your Chase account may get suspended.