Update: for a while now I’ve replaced Chase referral links on this site to those of my family members. I’ve also cashed out a good chunk of UR. I guess that tells you what I think my odds are.

Typically Chase credit card shutdowns were related to doing something like anonymous bill payment, selling points, and maxing out 5x categories through MS. But as of late DPs indicating new type of shutdown has been floating around and it has nothing to do with above listed reasons.

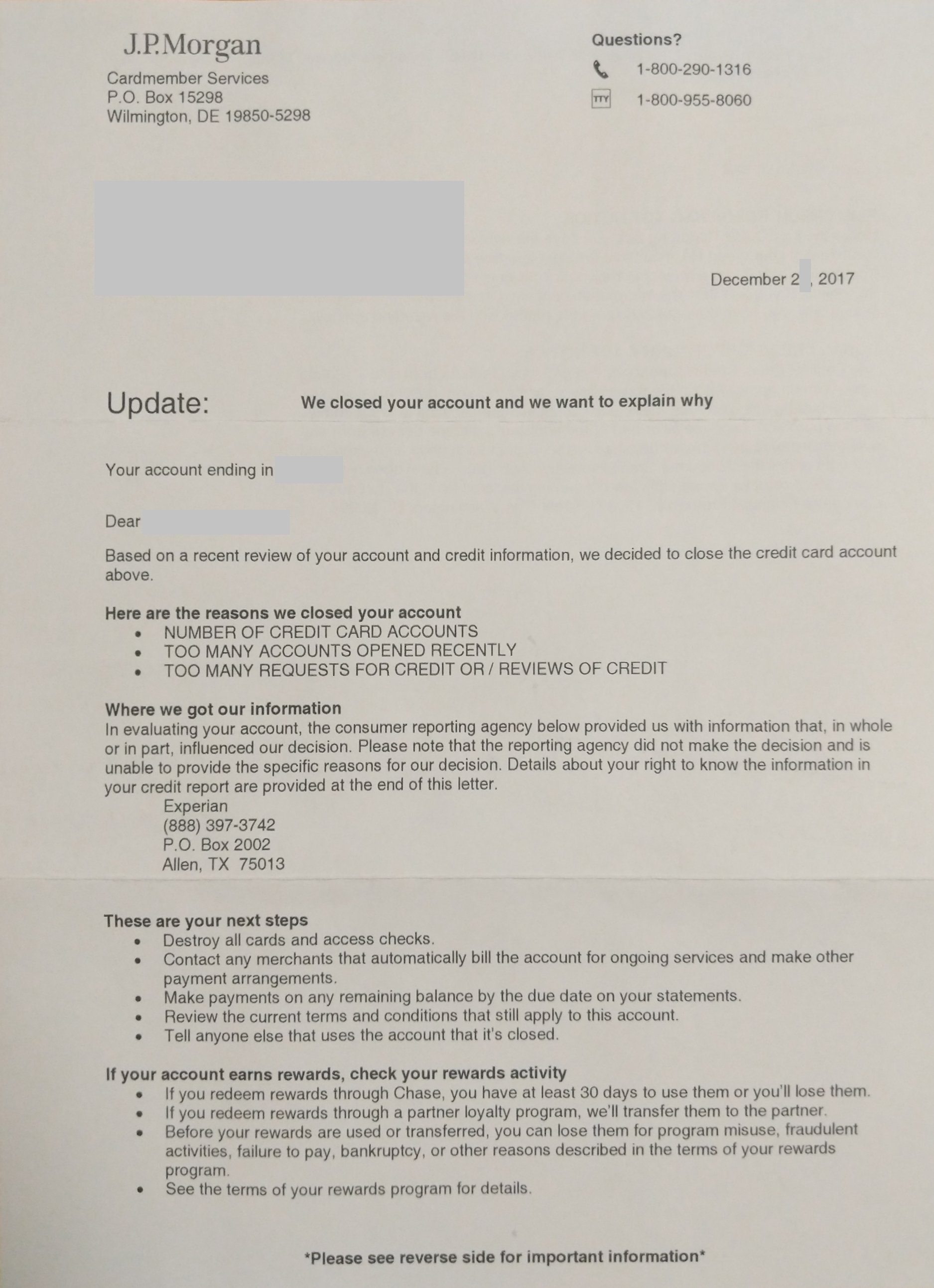

This new type of Chase shutdown is a result of the following:

- number of credit card accounts

- too many accounts opened recently

- too many requests for credit or review of credit

I’m not making this up nor am I making an educated guess on these reasons. Above listed reasons are the official reason given in the Chase shutdown letter.

So why does this matter and why is this a big deal?

Previously if you did not do fishy stuff like anonymous bill payment, selling points, etc then you were pretty much on the safe side. But this new reason for shutdown clearly indicates that even if you don’t do those things you may not be on the safe side.

However, there are two good news. First, decent number of these shutdowns have been reversed but the fact that not all were reversed is worrying. Second, 100% of these types of shutdown happen after one applies for a Chase credit card (business or personal does not matter).

I believe that when an analyst sees a messy credit report during review of a credit card application, s/he hits a “review this bastard” button and sends the file somewhere else to be reviewed. I believe they’re training analysts differently now otherwise reports of this type of shutdown would have existed a year ago.

Above hypothesis is supported by my own case as I was shutdown after several days of applying for a Chase card. How much is “several days”? This time span can shortly detailed as such (1) Chase send me a letter regarding my application (2) I sent Chase a response letter (3) Chase, having reviewed my letter, sent me another letter (4) few days later I call, sort everything out, and I am told that my application needs further review (5) a day or two later all my cards are shutdown. My point being, if it was automated I would have been shut within few days of Chase pulling my credit report. It was a clear case of someone reviewing my app and going “fuck this guy”.

How to Avoid This Shutdown

Banks change the rule and you must change with it. You must give up on the old ways and adopt with changing times. Unfortunately, when rules change some churners like me end up being the data point. Fortunately for you, here is my breakdown of how you can avoid same thing from happening to you:

- If you’re below 5/24, I strongly urge against rushing through Chase cards. Currently rushing through 5/24 is often advised for those who can’t wait to get out of 5/24, but because of this new form of shutdown, I now deem such advice to be ill-advised.

- If you’re below 5/24 and thinking of maxing out 5/24 cards to its full potential then I urge you to rethink. In other words, you should think hard before you plan on doing multiple of these – 2 x CIP, grabbing all 5/24 business cards, double dipping CSP and CSR, and double/triple dipping at 5/24.

- If you’re a post-5/24 heavy hitter, then you should flat out abandon the idea of applying for a Chase card. This includes forfeiting the idea of churning IHG, Hyatt, Ritz, etc cards every 24 months and getting pre-approved in branch.

- To summarize what I’ve said thus far – don’t be greedy like I was and don’t submit Chase app when your credit report has tons of new accounts and inquires. If you’re a heavy hitter and want to open a Chase card then I strongly urge you to take a roughly 6 month break before you submit an app and even then you may not be exempt from a shutdown.

I would also somewhat encourage people to

- reduce credit limit that has been extended to you. This does not prevent a shutdown since I’m someone who limits credit limit across all issuers and I still managed to get shutdown.

- get rid of duplicate cards. Do you really need a fourth freedom card? Sure you can have it but should you get shutdown, good luck explaining that to an analyst who could possibly override your shutdown.

- flat out decrease the number of Chase cards you have. Do you really need a MP card when you make MPX purchase once a quarter?

- not put all eggs in one basket and only go for Chase only. Seek credit elsewhere as well. If you’re a newbie to credit cards then Chase is likely to flag you even if you take 2 years to collect 7 Chase cards with no non-Chase cards in your portfolio.

- not get too attached to the idea of maxing out 5/24 slots.

Why Worry When Shutdown is Reversible?

A good portion of these shutdowns have been reversed but that does not mean you’ll have a positive outcome. Additionally one must keep in mind that the DPs on this type of shutdown have been in the range of 10-20 and we’ve only had a chance to peek at less than 3-4 irreversible shutdowns.

I recently saw a Chase shutdown DP of a regular churner with 10+ Chase credit cards and his shutdown was irreversible. This was the closest DP I had to mine and I thought to myself “if he had no change, what change do I have”?

I was positive that I could turn this shutdown around for myself but the further I talk with Chase the further I realize that this is a losing battle for me. However, I must say that 2 irreversible shutdown DP from regular churners does not prove all regular churners will be doomed in this case.

While I hope another regular churner in my shoe would have a better luck than I, the reality is that if you’re tons of inquiries and accounts then it is going to be really difficult to convince an analyst that you have any good intention. The only option churners like myself have is to be honest and admit that we’re just gaming status and points but that did not take me very far. I found that throwing in some keywords were helpful than other but maybe that is a topic for different day.

Anyway, to cut things short, my point is –

- if you can avoid being shutdown then why bother intentionally doing things that can lead to a shutdown even if it is reversible?

- generally speaking i think newbie churners with decent credit history will have good change of reversing the shutdown while regular heavy hitting churners will have very very very difficult time.

How is this Shutdown Different?

Long story short – I don’t know. Chase has been transparent to me about shutdown reason from day one but that is not like them. This made me believe that this is a “soft ban” and I should be allowed to get more cards in the future.

Also, Both my personal and business checking accounts are intact. When I asked if checking accounts would be shutdown, I was told something along the lines of “they haven’t been so far”. I have also been told by multiple chase representatives that I should be able to get more cards but when I questioned them on it, it was clear that none of them were certain.

I was sure that eventually Chase would welcome be back (i.e. this is a soft ban), well, until I received a letter stating why I was denied for the card I had applied for – “previous unsatisfactory relationship with this bank”.

I think this means that unless this ban is overruled (unlikely because of my profile) I’m done with Chase for life. It has been known that “previous unsatisfactory relationship” is known to eventually transfer over from credit card to banking and vice versa. Again nobody at Chase has confirmed this nor denied it nor have I seen a DP in this regard of anyone who has been shutdown for this reason.

P.S. if you’re new to this blog and curious about what cards I have, how often I churn, how rapidly do I apply, etc, then check my churning summary for year one (2016) and year two (2017). If that does not suffice, you may also check out Denials are Lessons #1, Learning from Denials #2, and Learning from Denials #3.

47 comments

Damn, sorry for that. That sucks.

I’m 6/24 and the annual fee for my ink+ is coming up. Instead of PC to CIC I want to apply for the 50k CIC offer. Now with all this going around I’m a little nervous. Especially my last three apps were:

7/7/17 – BOA Merrill

11/15/17 – Barclayscard JB+

11/20/17 – CIP thru BRM

The only DPs I haven’t seen are ppl applying thru BRM over 5/24 and being shutdown after.

Thoughts?

I think you’ll be fine. There have been no DP of someone getting shutdown post-BRM paper app. I assume this is because the application reviewers of BRM paper app aren’t trained to look for these details.

Now if somehow you were to be the first DP of this type, I think you would have a good chance of reversing the ban. An analyst is easier to persuade when you are 7/24 than you are at 20+/24.

Ultimately it is up to you to decide if the hassle of a possible shutdown is worth or not. If I was in your shoe I probably would have dropped the app but then again this whole mess happened because I dropped an app when I was lmao/24

Any idea if Chase was primarily concerned with churning *or* bust out fraud?

they kept referring to # of inquires i have and # of accounts i opened this year and even the last year. it was a pretty clear case of them booting away a customer who they think will max cc and run. funny enough i’ve had reduced CL to $500 on whole bunch of my chase cards lol

BTW, appreciate the DP and reflections.

Thank you for the heads up. There is a ton of info here; at the same time I am curious to see more details of your app history. The definition of “a lot” of apps will mean different things to different people.

Search for “year one of churning” and “year 2 of churning”. these posts detail out more or less everything you are looking for. if not enough, also search for “denials are lesson”.

DOH!, Yeah, I discovered this shortly after my post. Sorry… I just recently discovered your site.

no worries 🙂

I got hit with this in October. It was not reversed after appeal and review and CFPB review in the Executive office.

I did an AOR in October as a last hurrah to gear up for 5/24. It included a BA Visa that triggered the same shutdown letter. I called in and got a particularly nasty Chase rep that I think ratted me out.

I transferred all my UR to my wife which caused them to put eyes on her accounts and she got the irreversible axe too. So there’s that warning.

I’m not sure if this is a permanent ban or not. Executive office rep wouldn’t confirm it was permanent after CFPB. I just applied for a BA Visa again for fun. It’s in 7-10 limbo. I won’t be calling to check on it.

I do still have a Chase savings ($15k balance at the time) and a Chase auto loan that were spared.

Thanks for posting this. I’m well above 5/24 and the only thing I was going to do with Chase was reopen a Hyatt card I closed last year, but this post makes me focus on my reasons for doing so. I don’t REALLY need more Hyatt points at this time. Like so many people I’m on autopilot accumulating (and burning) points. Data points like this are very helpful. I’m holding off until there is a genuine need.

Sorry for your experience, but again thanks for blogging about it.

Thanks for writing up. It will be helpful to others.

Was Marriott Biz (the last chase app) the hammer that brought you the shut down?

If yes, then seems like both personal and biz cards are not spared from this.

yeap yeap.

Were you still able to transfer your points out? The 30-day language is pretty standard but this is a relatively new type of shut down.

no problem transferring or cashing out.

Thanks for the data point. Sorry for your loss. My thought is that your spouse got the evil eye from having the same household address, rather than your points transfer. Rats tend to gnaw on household members – whether they be significant others, parents or children.

RE: How to avoid this shutdown

What do you think would have happened if you didn’t respond to the first letter from Chase? You probably wouldn’t have been approved for the card but also probably wouldn’t have eyes put on your account thus not shutdown.

Agree?

an analyst eyeing my credit report lead to the shutdown.

[…] Lyft: Your 5-Star Reward is Here – 25%… Try the World – Canada Box Review Chase Credit Cards Closed for too Many Credit… Project Fi Bill Protection: Fi is Competitive Again… Simple Bank Still Relevant Because of […]

Damn. Just had a recon call with Chase yesterday for my 2nd ink (2 separate businesses) after reviewing my app I was questioned about my recent surge of chase cards including SWBusiness and personal in Dec and Sapphire in January. I made a good argument and felt like an approval was pending. CSR then suggested I could change products ( my SW bus for the ink and he would transfer me). Something told me I didn’t want to get into a battle of wits with specialized Chase reps to explain my tangled reasoning, I politely declined and told him I’d call back later. Just like your word of caution I slammed Chase after taking a break to get well under 5/24… I’m now glad I didn’t push the issue

I’ve read theories about Chase being concerned about flight risk leading to these types of shutodwns. Do you think having a long standing banking relationship (savings, checking, employer direct deposit) has an effect on this? I’ve read don’t “piss where you drink”, but I bank with Chase out of convenience and have churned a few cards. So far so good, but I will forgo the Marriott Biz card I was considering since I really don’t need Marriott points.

YMMV. Everything depends on the human who’s reviewing your file.

Any luck getting this overturned or any pointers for potentially getting this overturned. Just had all credit cards cancelled so going through the same process now. Thanks!

Hey John, the biggest tip I can give is to call the number on the back of the Ritz card (try CSR or CSP as well) and have them transfer you to a department that deals with risk assessment and shutdowns. Also, you should definitely read the two followup posts on this. You’re also welcome to email me (click on contact) or reach out via reddit or telegram.

best wishes

Hi thanks for the insights. Does product change trigger shutdowns? I am thinking of product change from CSP to CFU. Any risk of shutdown by downgrading a product?

Hey Sam, I have not seen any DP of shutdown being triggered due to PC. It should be okay to PC from CSP to CFU.

edit: saw a shutdown DP after PC..

[…] Chase Credit Cards Closed Due to Too Many Accounts and Inquires […]

“Unsatisfactory Banking Relationship” does not mean life time ban, unless Chase took a loss. Usually you can get back in with them after two years.

Also, I have heard that “tiggers” occur when you open four or more accounts within a one year period.

Yes, plenty of people with “unsatisfactory banking relationship” get back in through Ritz, but for some of them…when a human eye falls in their account, they meet the axe.

[…] after 6+ months from my Chase shutdown, I can still see couple of these cards when I login into my Chase account. A vast majority of my […]

Hello I wanted someone to look at my individual case and see if I have a chance for reinstated. I was recently approved for 2 chase cards after just having 1 card with Wells Fargo for 3 years. They approved me for the CSP 10k limit and the freedom unlimited 6.8k limit. Ive applies for some other cars and got approved as well. I wanted to take amazon up on their offer and applied for their rewards card not realizing it was issued by chase. Of course it was declined but a day later my cards stopped working and was told the accounts have been closed. I called but it was after business hours. What should I expect when I call in the morning. I’ve only had one of the new cards hit my credit reports which was discover. My utilization is under 11% at the moment and inquired on trans union is 5 and equifax 6 . I’ve spent a good amount of money on the csp card but have the cash and financials to back it up. I’ve only had the card for about a week. Is there hope for me? What did I do wrong?

Hard to say. I got hit last week after trying to open a MR visa account. I had two other Chase cards (SW and Disney). My utilization is ~ 4% and I have an 798 credit score. I called 800-290-1316 (Chase fraud department– these are the yahoos closing the accounts) and requested mine be reopened on 8/1 but have yet to hear back.

Funny thing is the MR visa arrived in the mail today along with three letters stating why my accounts were closed.

[…] had somewhat held off applying for new cards since my Chase shutdown because I wanted keep my report clean for a bit and also because doing so was likely the only way […]

[…] you might recall in December of 2017, Chase shut my credit cards due to too many recent inquires and accounts. Then in first half of 2018, my player #2 got all Chase […]

[…] you might recall in December of 2017, Chase shut my credit cards due to too many recent inquires and accounts. Then in first half of 2018, my player #2 got all Chase […]

This happened me a few months ago. Mine was reversed. I have all the chase cards I want, so that’s all well and good.

However, I’m now afraid to apply for cards from other issuers because I do not want to trigger another review by chase. The hyatt card is vital to me as they are my chain of choice.

So my question is, has anyone ever heard of chase shutting someone down based on new activity with other card issuers?

Thanks!

Chase claims they do periodic reviews but idk.

But there was a DP of someone getting shutdown after PCing a Chase card lol

Thanks for the reply. I think I’ll take a break, worrying about it stresses me out lol.

Agree that this is super-worrisome for those of us who actually stay a lot at Hyatt, but not mostly on OPM. Because: Hyatt card is now key to maintaining high status, and the link between UR points and Hyatt points is also crucial and something that can’t be replaced elsewhere, and the fact that Hyatt now lets points stays count toward requalification just makes the connection even stronger.

But without generating new UR points by sedulously going after new fundamental Chase cards in two-player mode, how to keep things going? Scylla and Charybdis!

Exact same thing happened to me earlier this year after I applied for Hyatt. I didn’t get instant approval, then it happened right after I called the reconsideration line. I was so mad that I called the Chase representative couple of times. I felt like they didn’t even know what “too many” is. They just kept repeating the same crap, such as you had been trying to apply for new credit cards (not just Chase cards, ALL kinds of credit cards) in a short period of time. Not so surprising, they didn’t give me an answer when I asked how long is “short period of time”. They transferred me to everywhere (to so called someone authorized) that I felt like I had spoken with the whole company. Isn’t this bank funny? When I said why should I be a high risk I never owe any bank a penny, they still kind of repeated the same thing, which they had been trained so well to do. They didn’t even let me close all my accounts myself. I was worried at the time since who knows how this is going to be shown on the credit report. Anyway, I felt the same, they are tough.

Like you, I was trying to develop long-term relationship with Chase. However, I terminated all my relationship with Chase after they did all this to me. I moved my money to another bank because I don’t think they deserve a penny, first of all. Second, I’ve got all my bonus long before this happened. That’s why I didn’t even feel sad or bad when this happened. I just thought it was unfair because I had been trying so hard to build my credit history and now someone is going to place a few stains on it for no reason. But now I’m doing way better with us bank and amex without any problem. Too many better candidates out there. Chase, just made me feel like it’s a bank that lures you with great perks and fancy packaging while it’s questionable whether they can really afford them. It’s just a sign that they are holding back on this to make their financial statements prettier. It’s not even related to risk control. It’s a show. After all, churners won’t bring in too much, but those who really come into APR will. Chase just needs a good reason to kick out whoever could possibly cause negative impact on their business. Well……

Hey Guys,

Curious about these as I just recently found out. I don’t consider myself a churner as in opening card, closing etc. However, I’ve had a few situations lately that I wanted some feedback on. Hopefully someone could give me some insights.

I currently have 1 inquiry on transuion and 3 on equifax. However, I’ve opened 3 cards since last November. 2 Amex hiltons as the ascend had some major issues when I got it, so I closed it roughly 6 months after getting it and opened the no annual fee card. I opened the new Marriott Card In july.

That has been all the cards I’ve applied for since 2016. I’ve closed 2 chases in the last 3 years. CSP when I signed up for CSR and Hyatt when I switched to SPG in 2016. Both of those closers were done in late 2016.

So here are my questions? 1. Will my canceling Amex hilton ascend so soon after it(roughly 7 months) affect me being able to get a Amex Aspire or Platinum? I really want a platinum, but I’ve kind of talked myself into an Aspire after staying at some Hiltons recently.

2. The only Chase card I want is World Of Hyatt as I’m going on a trip next year with some nice Hyatt Locations. Would you recommend on waiting? IF so when is enough Time? I have a inquiry fall off in December of this year.

I believe I’ll be set with cards if I can acquire Hilton Aspire, Platinum, World of Hyatt and Citi Prestige when it is launched. I rarely close cards and I’ve never Product Changed. In my entire life I’ve closed 8 cards? Best Buy, Care Credit, Amex Bluesky(all 7+ years ago) CSP, Hyatt and the Hilton Ascend that I some frustrations with at the time. I might have had a Chase card back in college, I think I did. So 9 in 20+ years and I tend to keep cards that I like. Hotel cards confuse me sometimes, because I like the annual night, but I bounce between chains. Anywho, sorry for the rambling. Just not being super into credit cards, going slow and using the points I acquire for a huge trip every 2 years and then small trips here and there is my preferred style, but I worry about the credit impact, the lack of credit limit etc.

On side notes I might have to buy a car soon(company switching from company vehicles to car allowance) and the reasons for the cards are to purchase engagement ring and plan a wedding/honeymoon!

Any help would be great!

[…] you might recall myself, player 2, and player 3 were shutdown by Chase for having too many recent accounts and/or […]

[…] my Chase credit cards were closed on December of 2017 but finally it looks like I’ve some chance of getting Chase cards again. […]

hi. Did you apply for other banks like amex after this? did it impact your application?

Hi Travelinpoints,

My chase reserve was closed yesterday and I didn’t realize until my purchases were declined. I recently ( about a week or so) upgraded my checking to Saphire banking to earn 60000 points by transferring 75000 new funds. I think this may triggered the shutdown. Looks like they only closed my reserve card, not the three other cards. I will call the number tomorrow morning, as the office was currently closed. I promptly transferred my UR points to one of my other card ( freedom) Actually I don’t think I did anything wrong at all. This is frustrating. They charged me Annual fee $450 last Oct. ,so far I haven’t got back all the travel creit ( $300) In case this account is not reinstated, Is there any chance that I could get the annual fee refunded? since I basically haven’t used the perks . Thanks for any pointers. BTW, great post.

Chase closed my 12 year old credit card (my oldest credit card to date) because I purchased nearly gift cards as birthday presents and too many accounts were opened and requested recently. Lending department said I can hear back after 10 calendar days. I hope my closed accounts get reinstated.

Were you reinstated?